- For yield-starved investors, preferred shares have been beneficial.

- The problem is many have chased yield and many preferred shares are overvalued.

- A careful look reveals there are many

preferred shares trading in excess of their call price - Lastly, many preferred share ETFs are skewed towards REITs and Financials – understand your sector exposures

It’s been difficult to find income and yield with global interest rates being suppressed by central banks and a lack of fiscal policy stimulus from the U.S. government.

It’s been a real tax on savers and investors that depend on fixed income to support their retirement. There’s nothing inherently wrong with preferred shares, but you need to look closely at the price you pay.

a. Preferred Shares Have Been a Solid Option

By keeping rates low, it was theorized, that investors would be forced into riskier assets. As a result we saw the run-up in Master Limited Partnerships – and their subsequent demise as oil and gas prices fell. We’ve also seen a run-up in preferred shares.

Below is a graph showing the performance of the iShares U.S. Preferred Stock ETF (PFF) for 2016.

It shows two things:

(i) high volatility with a decline of 8.5% to a low of 35.89, followed by a run-up of 12.4% from the February low; and

(ii) a good overall return with a year-to-date return of over 9%, both capital appreciation and dividends (current annual yield is about 5.6%).

(Source: Charles Schwab)

Jason Zweig points out in a recent Wall Street Journal article that PFF, which seeks to track the preferred stock index market, has taken in $2.2 billion in new money so far this year.

This inflow of new capital is likely the reason that the price of preferred stocks has risen, which almost never happens with most of their return coming from their fixed dividends. This year, however, almost half the 9% total return of the S&P preferred index has come from rising share prices.

b. Many Have Chased Yield and Many Preferred Shares are Overvalued

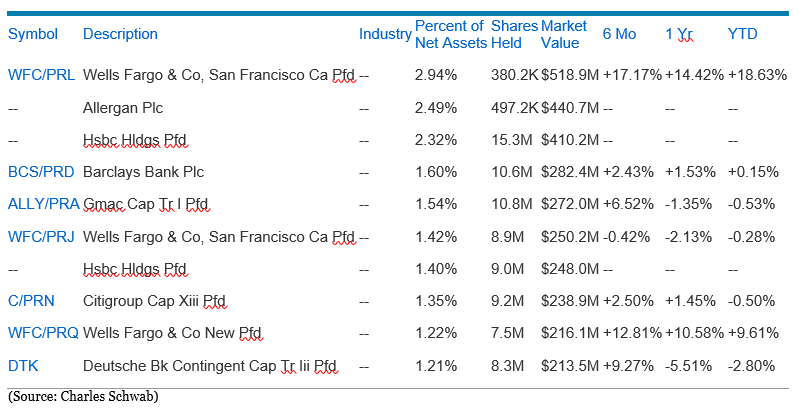

The top 10 holdings of PFF show a few things. First, nine of the top 10 holdings are financials, which represents a significant sector overweight.

Next, you can see the run-up six month returns driven by a demand for yield from yield starved investors. What you don’t see is the largest single holding is actually cash standing at 3.6% of PFF’s portfolio.

Investors are unaware of the differences between preferred shares, common equity and bonds. One key difference – preferred shares are often callable. In fact, 28% of PFF’s $17.5 billion in holdings are callable by the end of 2016, according to Jason Zweig.

Issuers of preferred shares have the right —not the obligation — to redeem those securities, taking them off the market in order to refinance at lower rates.

The threat of rising interest rates suggests that many of these callable preferred shares will actually be called at, typically, a price of $25.

c. Many Preferred Shares are Trading in Excess of Their Call Price

For Example, GMAC Cap Pfd shares, currently trading above $25.20 are callable on September 18, 2016 at a price of $25.

Jason Zweig points to another good example. He highlights the $950 million in preferred securities from Bank of America’s Merrill Lynch Capital Trust II, whose price shot up from $25 in February to $26.50 in June, far above the $25 par value.

Then, in July, the bank announced it would call the securities on August 15, 2016. Their price fell 2% in a day. This was one of PFF’s largest holding in July 2016.

d. Many Preferred Share ETFs are Skewed Towards REITs and Financials – understand your sector exposures

About 80% of preferred shares are issued by real estate investment trusts, banks and other financial companies.

Investors need to understand that they are not just gaining exposure to a ‘different financial product’, but they could be unwittingly increasing their exposure to real estate investment trusts, banks and other financial companies.

IMPORTANT NOTE: This blog is for informational purposes only and comments will not be posted on this site.

[1] Article by Jason Zweig (Wall Street Journal August 12, 2016).

[2] Jason Zweig (Wall Street Journal August 12, 2016).

[3] Jason Zweig (Wall Street Journal August 12, 2016).